Is Florida in for a crash like in 2008?

Sarasota, FL - The real estate market crashed 2007/2008, so it will probably happen again, right? Let's dive deep into the differences in today's Sarasota real estate market.

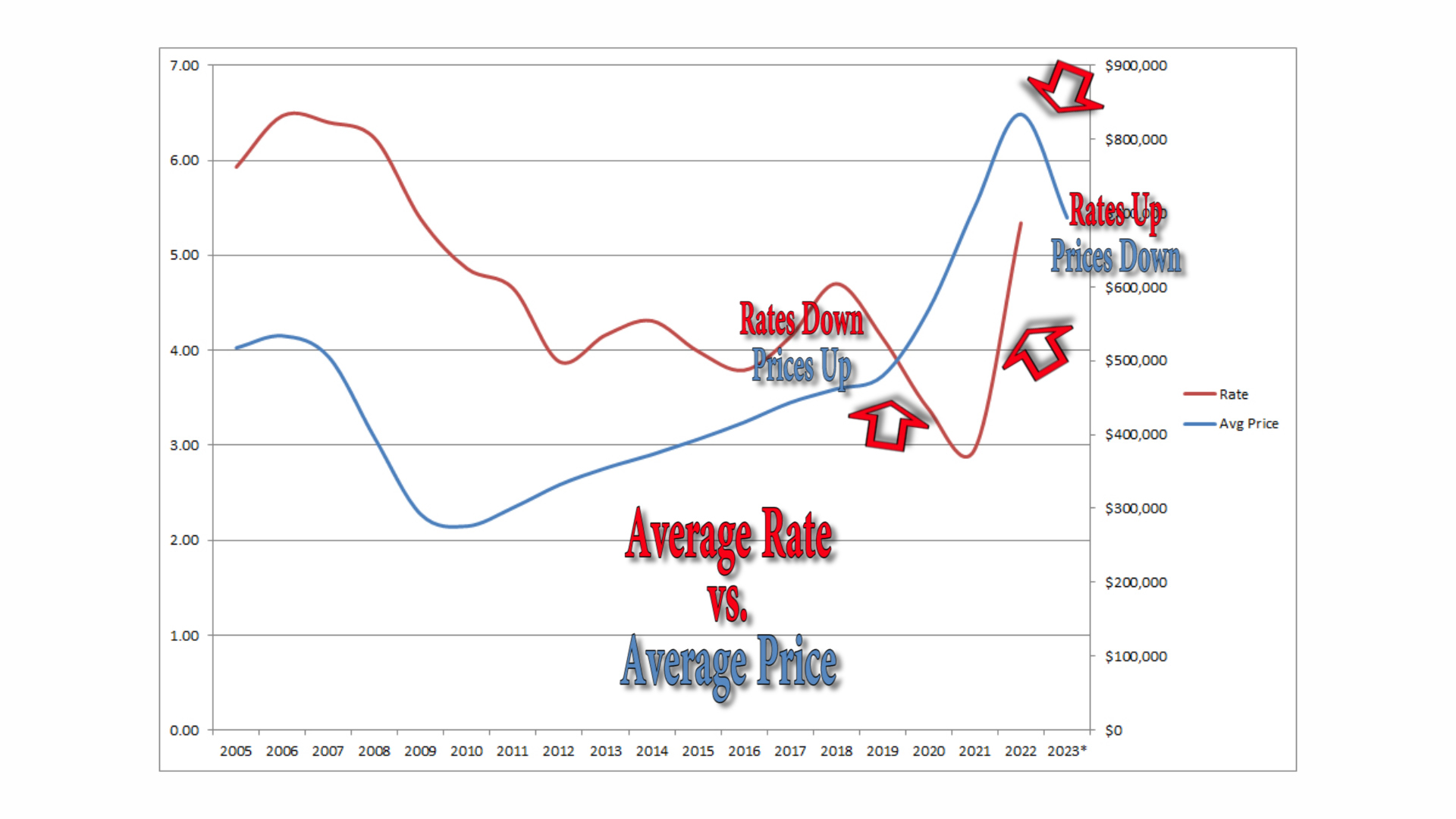

The most significant comment I hear from people looking to buy is that they are waiting for prices to come down or the market to crash. The price increases we saw over the past few years were spectacular and, of course, not sustainable. Interest rates began to increase in early 2022, putting the brakes on an overheated market. The first thing many start thinking is that the market will crash, as it did in 2008. The foundation or runup to the crash of 2008 vs. today is quite different, and a crash is doubtful.

Be Sure To Check Out Our Video

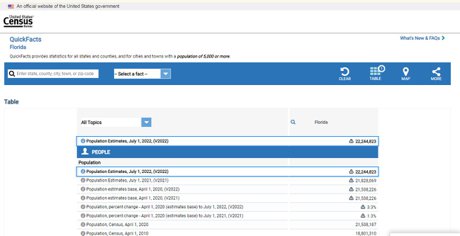

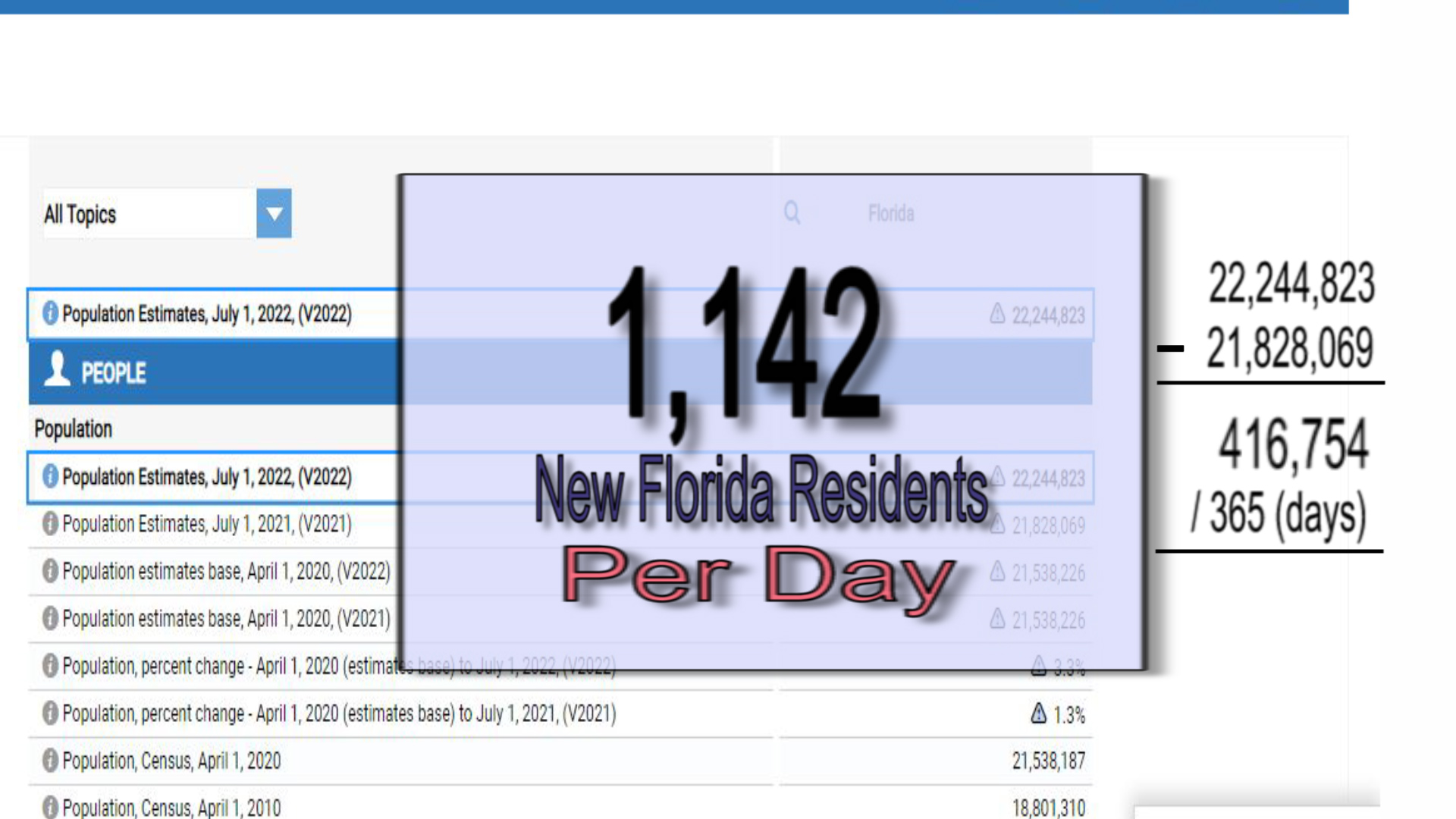

Florida is a desirable destination due to the warmer climate. Supply and demand govern market prices. Low-interest mortgages allow homebuyers to pay higher costs when money is cheap and helps to increase demand. We also have no state income tax, and there is a general feeling that Florida is a well-run state. The US Census reports that Florida is the fastest-growing state since 1957. Pair that with the ability of the workforce to work remotely, and it is no surprise that between 800 and 1,000 new people become Florida residents every day. Demand remains strong at all price points, including the luxury Sarasota real estate market.

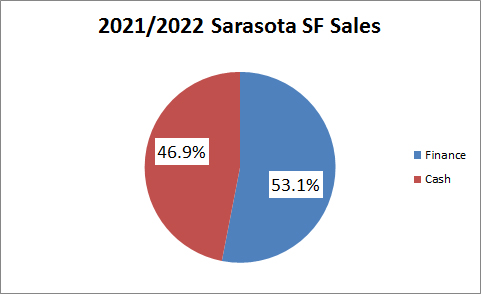

Home purchases over the past several years are evenly split between all cash or finance purchases. In the years leading up to 2008, cash purchases were only 15% of the total sales. Financed homes today typically have larger down payments than the loans before 2008, so owners of the financed homes have "more skin in the game."

The lessons of the 2008 crash eliminated "80/20" loans. Essentially, these were 100% financing. "Pick-a-pay" and negative amortization loans were also common. Home prices rose because mortgages were easily obtained with little or no money down and lax borrowing standards. The thinking was that rising prices would offset increased mortgage balances common with negative amortization loans. However, when values level off or go down, the losses accumulate quickly, and markets do not go up forever. When prices started to level off, owners found themselves upside down. Many decided to leave these properties and let the bank take them back through foreclosure. It turned a cyclical market correction into a catastrophe by adding a glut of short sales and foreclosures to the supply. With half of the homes over the past several years bought for cash or financed with higher down payments, the underlying foundation of this market is much stronger than the years before the 2008 crash. Just remember, interest rates were around 6%, as they are today.

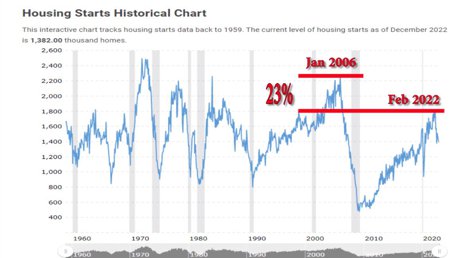

Another unmentioned carryover from the 2008 correction still affects today's market is new home construction. It peaked at 2,273,000 starts as of January 2006. The most recent peak was just 1,777,000 home starts in February 2022. Housing starts are about 23% below 2008 levels. Post-COVID supply chain issues linger and restrict supply. Demand for building materials in portions of South Florida still exists due to the recovery effort from Hurricane Ian. In other words, the supply of new homes has yet to achieve the levels in 2007.

As reported by CNN, we are not building enough homes in the US to meet the growing population. Increasing demand that exceeds supply is what pushes prices up.

Still, Florida is the #1 state for net population gains from the 'Great Migration.'

Again, the balance between supply and demand dictates market prices.

According to The US Census Bureau report released in December, Florida was the fastest-growing state in 2022. The mistake some are making is that if national real estate sales numbers are down, Florida must be down too. Florida has certainly slowed, but market prices are relatively flat due to supply and demand. The current mortgage rates hold prices back, but the supply and demand balance keeps prices from falling. The effect of a slowing or "more normal" market is that multiple offers and bidding wars are less prevalent than in 2021. Buyers can negotiate and finance and do not have to waive inspection or appraisal contingencies. Even so, I regularly see some homes go pending in a few days and several buyers I have that are waiting for inventory in specific areas to become available. Sellers are generally negotiating, but there are areas within our very diverse market with bidding wars because of tight supply.

market is that multiple offers and bidding wars are less prevalent than in 2021. Buyers can negotiate and finance and do not have to waive inspection or appraisal contingencies. Even so, I regularly see some homes go pending in a few days and several buyers I have that are waiting for inventory in specific areas to become available. Sellers are generally negotiating, but there are areas within our very diverse market with bidding wars because of tight supply.

Marketing times are usually longer, which allows buyers time and leverage they did not have last year. Market inventory in January was 2.8 months instead of 0.6 months in 2022. A balanced market has about six months' supply.

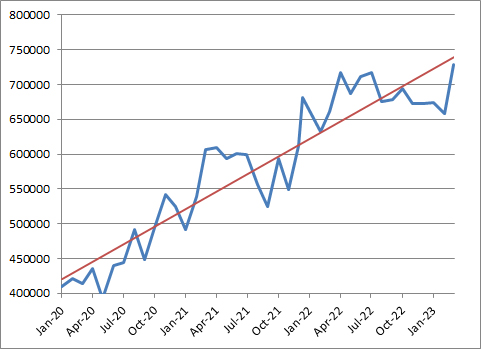

The broad Sarasota area market peaked in July this year with an average sales price of $717 398. December's average price was $672,688. The average for January 2023 has inched up to $674,468.

While financing costs more, meaning a higher payment, buyers can negotiate price and closing costs. That can offset some of the increased amounts.

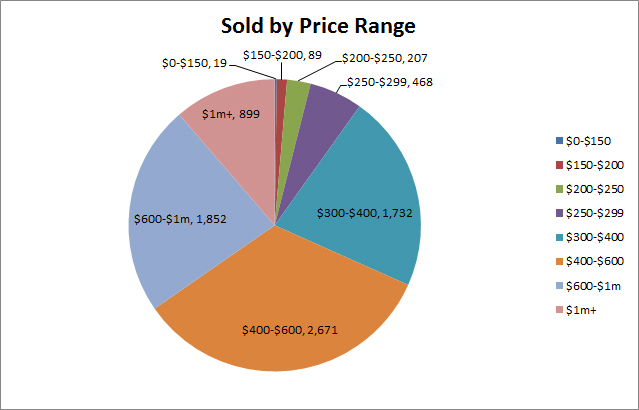

Every situation is unique, and Sarasota has several markets due to the economic diversity of the population. Broad market numbers are interesting, but analysis of your specific market helps avoid leaving money on the table. Sellers are generally the last ones to get the memo that prices are not up like they were and tend to price their homes high, so there are many price reductions. That is what I do.

Time is always a factor when selling. When a price is above market and sits when a market is flat or declining will always leave a seller with less than if the home was priced correctly in the first place. If the market declines, quick and decisive adjustments are necessary to avoid chasing the market down. On average, sellers will sell in 30 days or less once pricing is in line with the current and not a "hoped for" market.

Comparing short and longer timeframes of supply helps to understand where the market direction. Stats of the market are usually two months or an entire quarter behind where the market is. Here is a screenshot of the 7-day market view critical to understanding the "now" market compared to a longer-term view. Add the new and 'back on the market' counts and subtract pending, expired, withdrawn, and canceled categories. Sold properties do not count because all properties become pending before being sold, and price changes don't affect inventory levels. This is one of the areas of the market I track and helps me keep buyers and sellers best advised. The supply decreases if the number is negative; positive numbers mean more inventory. In this case, the active market has had 68 fewer (or about 4% less) active listings over the past seven days. 4%, four weeks in a month, and in theory that is 16% fewer homes which, in this case, is significant.

In many ways, buying a home now is more accessible than a year ago. Last year, there were 15 offers for every home, meaning 14 people came away frustrated and empty-handed. We are hopeful rate hikes are ending as it would help stabilize confidence. Higher rates tend to push prices down, but with a higher interest rate and lower price, the overall cost of ownership is not significantly different.

In many ways, buying a home now is more accessible than a year ago. Last year, there were 15 offers for every home, meaning 14 people came away frustrated and empty-handed. We are hopeful rate hikes are ending as it would help stabilize confidence. Higher rates tend to push prices down, but with a higher interest rate and lower price, the overall cost of ownership is not significantly different.

Waiting for rates or prices to come down is generally not a productive path to a better deal. If rates go up, prices flatten or retreat. Declining rates tend to allow prices to go up. In either case, the overall finance cost either doesn't change or increases.

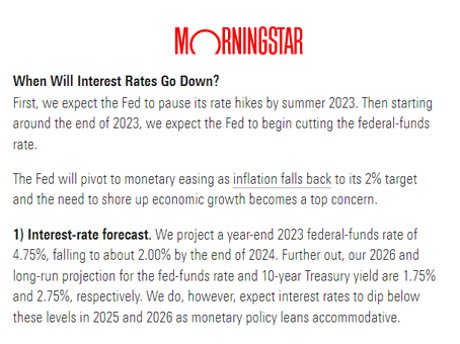

Locking in a price now and waiting a few years to refinance at a lower rate could give you the best of both worlds. Remember, lower rates are a factor in allowing prices to rise. Some analysts predict the FED will lower rates by as much as 2% by year's end. A lower price today and a better refinance rate tomorrow are something to consider when buying now.

Feel free to leave a comment below, or if you have any questions, please reach out to me, and I'll be sure to get you answers.

I'm John Woodward, and you make it a great day.

Join In the Discussion Here